Congress Looks at Excessive Swipe Fees

“The credit card market is an antitrust problem, and there is plenty of consumer harm to prove that,” NACS testifies.

May 05, 2022 | 4 min read

WASHINGTON—NACS called on Congress yesterday to bring competition to the U.S. credit card market, saying decades of domination by Visa and Mastercard has shut out innovation and led to soaring swipe fees that are a burden for small businesses, drive up prices for consumers and contribute to inflation.

At a Senate Judiciary Committee hearing on swipe fees, NACS General Counsel Doug Kantor testified on behalf of the convenience store industry and the Merchants Payments Coalition (MPC), of which NACS is an executive committee member.

In his opening statement, Kantor described the antitrust issues borne from Visa and Mastercard’s dominance of the credit card market. “This is an incredibly concentrated market, and none of [the banks] are setting their own prices. That doesn’t make any sense,” stated Kantor. “On top of that, Visa and Mastercard set the terms by which cards are accepted, which make sure to insulate those fees from any other competitive market pressure to make sure they can stay high.”

Kantor testified at the Senate Judiciary Committee hearing on “Excessive Swipe Fees and Barriers to Competition in the Credit and Debit Card Systems,” called by Committee Chairman Dick Durbin, D-Ill. after Visa and Mastercard last month refused to withdraw a $1.2 billion increase in swipe fees.

Durbin, Sen. Roger Marshall, (R-KS), Rep. Peter Welch, (D-VT) and Rep. Beth Van Duyne, (R-TX) wrote to Visa and Mastercard last month asking the card companies to withdraw the rate hike. The lawmakers said the increase would add to inflationary pressure and is the “last thing American families deserve right now.”

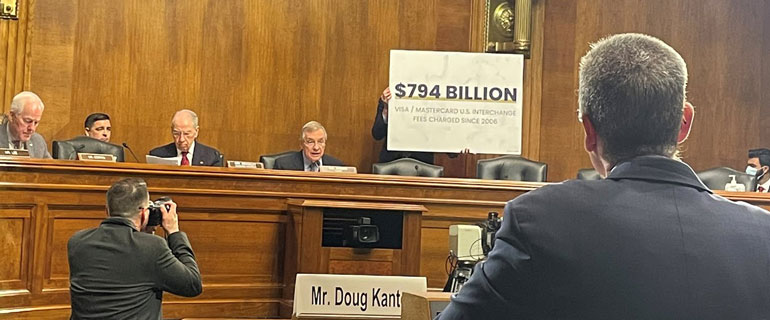

In his opening statement, Chairman Durbin remarked that it was the first time the Judiciary Committee had held a hearing on the topic since 2006, and swipe fees had increased $794 billion since then.

“When Visa and Mastercard raise interchange fees, banks want to issue more cards because they make more on each swipe. And Visa and Mastercard profit when there are more swipes, because they take their own cut, called a network fee, from the merchant on each swipe. But merchants and their customers take it on the chin,” stated Durbin.

Credit card swipe fees remain one of the highest operating costs for convenience store retailers after labor, according to NACS State of the Industry data. In 2021, overall card fees paid by the convenience store industry were $13.5 billion, up 25.6% in 2021 versus 2020 ($10.7 billion), NACS SOI data indicate.

During the hearing, when asked how consumers are impacted by the increase in fees convenience stores have experienced, Kantor responded, “There is 100% pass through of both cost increases and cost decreases from fuel prices into the retail cost of gasoline, so these fees without question get paid by consumers every day.”

Kantor noted that U.S. merchants paid $138 billion in credit and debit card processing fees in 2021, a “huge jump” from the $110.3 billion paid the year before.

“One of two things is happening when the credit card industry argues that consumer prices and retailer costs don’t flow through—either they don’t believe competitive markets work, or they’ve been living so long with centrally setting the fees that they’ve forgotten how competitive markets actually work,” he said.

At a time when Americans are experiencing the highest inflation in 40 years, the card networks are benefiting from it. Durbin noted that in Visa’s last two earnings calls, the credit card giant shared that it is a beneficiary of inflation.

“We need to deal with the competition problem in credit cards to have a fair deal for merchants and consumers, and frankly for the U.S. economy,” stated Kantor. “When we have competition, prices are lower, we have more innovation, and people have more money in their pockets. They can spend more, and that consumer spending helps drive the economy.”

Swipe Fees Credit