Buy Now, Pay Later Providers Move Focus to Physical Retail

With e-commerce spending plateauing, BNPL providers are hoping physical retail will net more users.

Feb 16, 2023 | 4 min read

ALEXANDRIA, Va.—Buy now, pay later (BNPL) services are setting their sights on physical retail to drive business as e-commerce sales remain stagnant, repots Modern Retail.

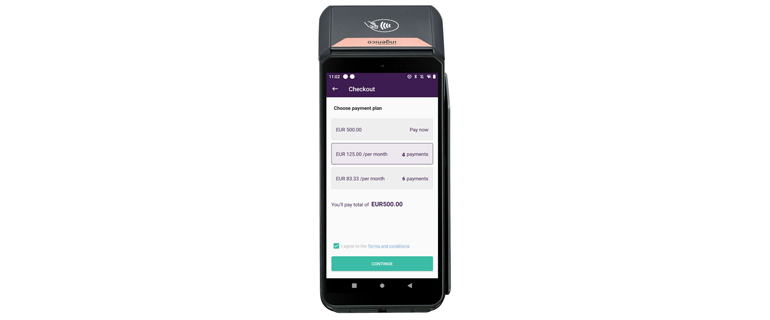

Splitit, a white-label BNPL provider, is now offering physical retail customers the ability to sign up for payment plans at checkout without the customer having to sign up for any third-party payment provider. Splitit has teamed up with Ingenico to offer the service.

“Many of our merchants want to offer an omnichannel experience for their installment services,” Nandan Sheth, Splitit CEO, told Modern Retail. “Unlike the more legacy traditional BNPL cells where there is a new loan originated and we have to go through a seven-step registration and underwriting process … our experience is zero friction, fully embedded.”

There are no fees if a customer chooses to sign up for a payment plan through Splitit, which uses existing credit that the shopper has to charge the shopper in installment payments. This is a different business model than some other BNPL providers, that underwrite new loans for purchases.

“If you look at the traditional BNPLs, they’ve really not even scratched the surface of point of sale, because their experiences are multistep, requiring an underwriting of a loan,” Sheth told Modern Retailer. “We don’t have any of that. If we execute on this relationship, we could very easily become the market leader for point of sale installments with this partnership.”

Splitit earns profits through a subscription-based service it charges the merchant. Sheth told Modern Retailer he believes that the new offering will give retailers an edge over their competition because customers won’t need to sign up for anything or create a new account.

“If you think about the size of the market, and the merchants’ need to have a frictionless experience, the demand is massive,” he said.

According to a PayPal-commissioned survey, 79% of millennial and Gen Z BNPL users were more likely to make repeat purchases at a merchant that offered the service. Forever 21, for example, offers BNPL options for customers via BNPL companies Klarna and Afterpay. The company’s chief marketing and omni-channel officer told Modern Retailer that the implementation of BNPL in stores has been successful.

“For some customers, it’s just a different form of [credit], whether it’s Klarna or Afterpay,” he said.

Klarna and Affirm, another BNPL service, released debit cards last year that allow users to split their purchases into smaller payments without any interest. Affirm CEO Max Levchin told shareholders in a letter that its debit card is a “high conviction bet.” He also said the company is working to “fine-tune its unit economics.”

A recent New York Times article found that with historically high grocery and food costs, more consumers are turning to BNPL methods to pay their weekly food bill. They’re even using these options for smaller purchases such as coffee or a sandwich.

One BNPL user told the Times she doesn’t hesitate to use the service for her everyday food purchases.

“If I wanted to pick up a coffee on the way home from somewhere and I didn’t have any money in my coffee or eat-out budget, I would push it to next month’s budget,” she said.

BNPL companies tout the convenience of their services and how they help consumers through difficult financial times.

Walmart is reportedly launching a BNPL service for customers through a fintech company backed by Walmart. The company, called One, is majority-owned by Walmart, and the service could be available as soon as this year.

Payments Dive recently reported that the Consumer Financial Protection Bureau is considering new rules for BNPL methods to ensure BNPL providers are adhering to laws that apply to credit card companies.

New rules could include disclosure requirements on the transactions to increase consumer transparency, as well as dispute protections for users, requirements for reviewing a borrower’s ability to pay and reasonable penalty fees.

Payment