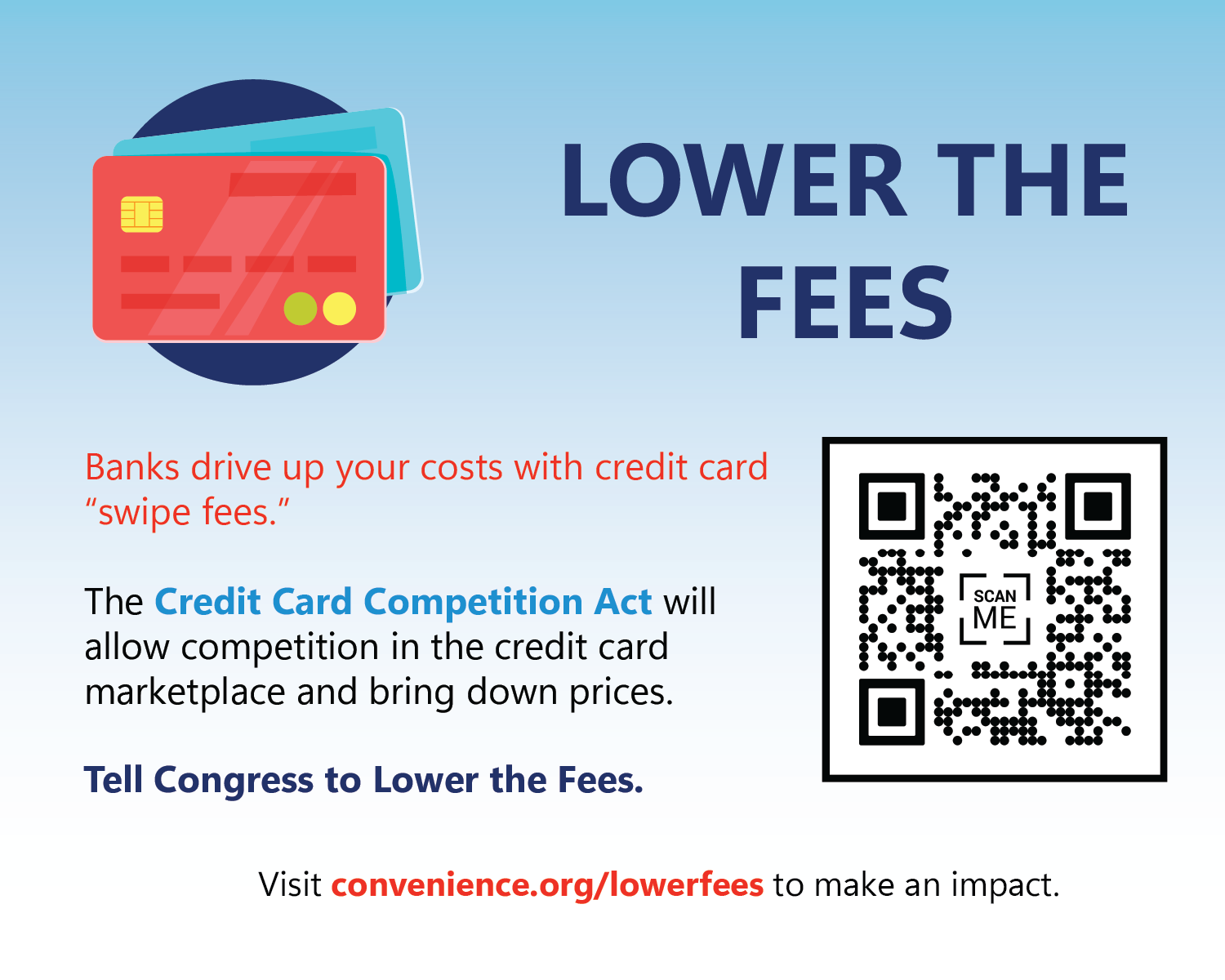

Credit Card Competition Act

The Credit Card Competition Act would inject long overdue competition in the credit card market, requiring Visa and Mastercard to compete on fees and services.

The Issue

The use of credit cards comes at a hidden cost to main street businesses and their customers. Every time a payment card is used, fees are charged to the retailer, and those fees have been rising at a dramatic rate for a generation. Because credit card fees are a percentage of the total transaction cost, they multiply with every cent of inflation, driving up the cost of every good and service in America.

The reason these fees are far higher than a free market should bear is because two dominant players—Visa and Mastercard—control about 83% of the credit card volume and price-fix the fees that their card issuing banks charge retailers. Banks should compete on their swipe fee prices, but they all agree not to do that. Retailers have no choice but to accept these cards, meaning they are stuck with whichever network is on the card. This results in swipe fees increasing year after year and U.S. merchants and consumers paying more in such fees than the rest of the world. The market is clearly broken.

Retail Impact

The U.S. convenience store industry has more than 152,000 stores, 60% of which are single-store operators. These businesses have seen a historic jump in their swipe fees with inflation and rising gas prices. In 2024, convenience stores paid $21 billion in swipe fees, up more than 80% since 2020 alone. For many in the c-store industry, the swipe fees they pay exceed their pre-tax profits. These fees represent their second-highest operating cost—less than labor but more than rent and utilities. On Visa and Mastercard credit transactions, the average rate paid in the United States was 2.36% of the transaction amount—more than 7 times what merchants pay in Europe.

The Credit Card Competition Act is a Market-Based Solution

The Credit Card Competition Act (S. 3623 and H.R. 7035) was introduced by Sens. Roger Marshall (R-KS), Dick Durbin (D-IL) and Peter Welch (D-VT) in the Senate, and Reps. Lance Gooden (R-TX-5), Zoe Lofgren (D-CA-18), Tom Tiffany (R-WI-7) and Jeff Van Drew (R-NJ-2) in the House. The bill has been endorsed by President Trump.

The bill would bring long-overdue competition to the credit card marketplace by creating a choice for the processing of credit card purchases. It would ensure the largest U.S. banks that issue Visa or Mastercard credit cards allow transactions to be processed over at least two unaffiliated card payment networks—the same process that has been used for debit card transactions for more than a decade. CMSPI, a payment consulting firm, estimates that credit card competition would save American consumers and businesses more than $17 billion per year. For the c-store industry, that would mean about $10,000 per year in savings for each convenience store across the nation.

NACS Position

NACS supports this legislation because businesses like convenience stores thrive on competition, and the card networks should too. It’s time for Congress to pass this bill and bring competition to credit cards through market-based reforms.

Download material to use in your store to inform customers about swipe fee reform.

Doug Kantor

General Counsel

NACS

(703) 518-4228

Doug Kantor joined NACS as its General Counsel in May 2021.

Prior to that, Kantor most recently served as a partner at Steptoe & Johnson LLP. In this role, he worked with a range of clients, including NACS, to address public policy issues ranging from fuels to financial services. Kantor also established and administered coalitions of companies and trade associations that share common legislative and regulatory objectives. During his tenure at Steptoe, Doug also served as counsel to the Merchant Advisory Group, Society of Independent Gasoline Marketers of America, National Grocers Association, National Retail Federation, Merchants Payments Coalition, and Main Street Privacy Coalition, among other groups.

Kantor’s legal experience includes appellate litigation, campaign finance law counseling, privacy law counseling, defending state attorney general investigations, litigating securities enforcement actions, and class litigation.

Prior to Steptoe & Johnson, Kantor practiced at Collier Shannon & Scott PLLC. He also served as Special Counsel & Deputy Chief of Staff at the U.S. Department of Housing and Urban Development. Prior to attending law school, Kantor served as a public school teacher.

Kantor received a B.A. from the University of Virginia and a J.D. from Yale Law School.